Most families think of inheritance as a question of ownership. Someone dies, the documents are produced, and the assets pass. That assumption holds well enough when the owner, the heirs, the assets, and the legal system all sit in the same country.

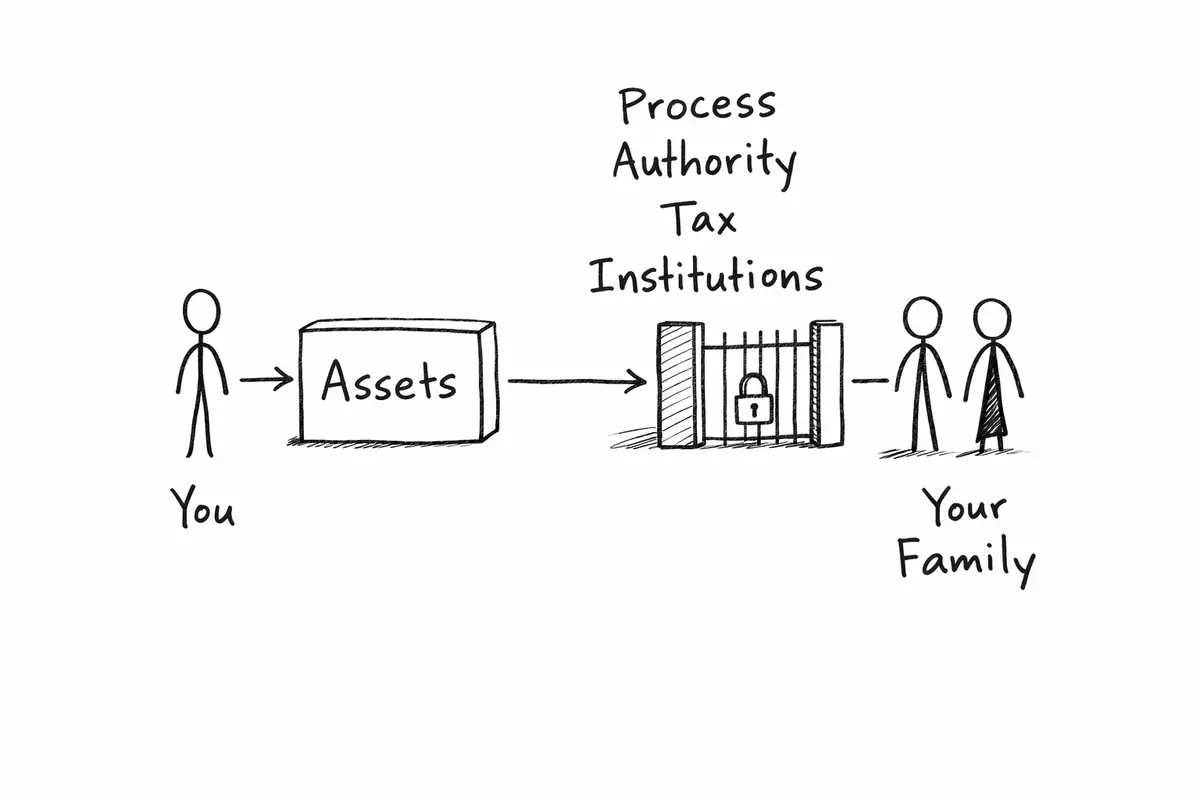

It becomes less reliable when U.S. assets sit inside an international family. In that setting, the heirs are not simply receiving wealth. They are receiving a U.S. system that decides how authority is proved, which documents are acceptable, whether tax procedures have to be addressed, and when an institution is willing to release control. That does not mean every family faces a tax problem. It does mean cross-border inheritance is often much more of an operating problem than families expect.

Consider a common case. An American executive has lived in Vietnam for years and keeps a U.S. brokerage account. The account is dollar-based, familiar, and often more convenient than local alternatives. His wife is Vietnamese. His children may hold different passports depending on where the family has lived. During life, the account behaves exactly as it should. Statements arrive, advice is taken, trades can be made, and everyone regards it as part of the family’s wealth.

The risk hides in that ordinariness. Nothing in the owner’s day-to-day experience tells the family how the same account will behave once the owner is gone. At that point, a surviving spouse living abroad may be dealing with funeral arrangements, household expenses, school costs, and several advisers at once, while the account itself is being recast from an investment account into a U.S. estate asset. I have seen families wait many months, sometimes with a will already in place, because legal entitlement and usable control turned out to be two different things.

International estate planning often fails because it is designed from the wrong vantagffe point. Owners can answer what they own, how accounts are titled, and whom they want to benefit. The surviving family often cannot answer the questions that matter just as much once a death occurs: which assets pass by beneficiary designation, which require probate or trustee action, which institution holds the account, what that institution accepts as proof, whether the executor is local or foreign, and who is expected to keep the process moving. A structure can therefore look orderly during life and still become clumsy at the first moment it is tested.

Domestic estates are more forgiving. The legal system, the people administering the estate, the institutions holding the assets, and the documents proving death or authority usually belong to the same country. Families can learn part of the process as they go. Cross-border estates remove that luxury. A death certificate may be issued in one country, probate authority may arise in another, the custodian may sit in the United States, and the family may need tax advice in two or three jurisdictions at once. None of this is exotic. It is simply cumulative.

The failure point, then, is rarely the absence of planning language. Wills, trusts, and beneficiary designations matter, but they are not self-executing. The plan fails when a person who is entitled in principle cannot act in practice. Many plans look complete because the documents exist. The more revealing question is whether the heirs can turn those documents into action without discovering the system for the first time in the middle of bereavement.

U.S. assets create extra friction because they bring a U.S. legal and institutional framework with them. Once a U.S. brokerage account, U.S. real property, or other asset legally situated in the United States enters estate administration, the governing questions are no longer only familial or economic. They become legal. Who was the decedent for U.S. tax purposes: a citizen, a domiciliary, or neither? Where does the asset legally sit? Did it pass by beneficiary designation, trust, or probate? Is the surviving spouse a U.S. citizen? Those questions are not answered simply by saying the family lives abroad.

Many international families think of residence and jurisdiction in ordinary-life terms. They live in Vietnam, Singapore, Dubai, or London, so the estate feels international but not especially American. The U.S. system does not reason that way. It classifies by legal status and asset type. An owner can spend decades abroad and still leave the family with a very U.S. transfer problem. In the same way, assumptions that feel ordinary in a domestic estate do not always carry across the border unchanged. A surviving spouse who is not a U.S. citizen, for example, can find that the tax treatment is not simply the domestic one transported overseas.

Institutions add another layer. Investors experience a U.S. brokerage account in financial terms: performance, liquidity, allocation, custody. The institution experiences it procedurally once the owner dies. It asks who has authority to act, what documentary standard has been met, what filings must be addressed, and whether the intended recipient can be onboarded at all. For a non-U.S. beneficiary of a U.S. brokerage account, the practical problem is therefore rarely “Do I inherit?” It is “What must I prove, to whom, in what form, and how long will that take?”

None of this means U.S. assets are a mistake for internationally mobile families. Often they are entirely sensible. The point is narrower. U.S. assets tend to come with a more formal transfer environment than families expect, and that environment appears at the precise moment the people who have to satisfy it are the ones least prepared to do so.

Once a death is reported, the process usually begins with restraint, not release. Access is limited, standing instructions may stop, and the account moves into an estate or inheritance workflow. That is reasonable from the custodian’s point of view. The institution is being asked to change control of property after a death. But it is also the moment many families first discover that what looked liquid on a statement is no longer liquid in the ordinary sense.

From there, three separate gates tend to appear. They are related, but they are not the same. The first is proof of authority. The second is tax clearance. The third is the institution’s own release process.

Proof of authority comes first because the institution needs to know whom it can listen to. If a beneficiary designation is valid and operative, the path may be shorter, although not frictionless. If it is not, or if the asset sits inside a trust or probate estate, the institution may need to hear from an executor, administrator, or trustee. This is where families learn the difference between intention and authority. A will may explain what the deceased wanted. It does not necessarily empower the person calling the brokerage firm to move the account. In practice, firms often ask for some combination of a certified death certificate, letters testamentary or letters of administration, trust certificates or extracts, identification documents, beneficiary forms, and new account paperwork. If the asset must be administered through an estate, an estate account with its own tax identification number may also be needed before receipts and distributions can be handled cleanly.

The difficulty increases when the core documents were issued outside the United States. A foreign death certificate may be perfectly valid where the death occurred and still be insufficient for U.S. estate administration in the form first presented. A firm may ask for certified copies, an English translation, an apostille or other legalization, or additional evidence linking the foreign document to the person whose U.S. assets are being claimed. Foreign probate papers can raise the same issue. None of this is universal. Requirements vary by institution, by state law in some cases, and by the facts of the estate. The problem is that heirs usually do not discover the specific standard until they are already inside the process.

Tax clearance is a separate question. Whether U.S. estate-tax procedures matter depends on who the decedent was for U.S. purposes and on the type and location of the asset. For some estates, that means a Form 706 or Form 706-NA filing. For a surviving spouse who is not a U.S. citizen, assumptions familiar in domestic planning do not necessarily carry across unchanged. In some nonresident cases, transfer-certificate procedures can also enter the picture before a U.S. institution is comfortable releasing or retitling property. Not every estate will face that step, and it would be a mistake to imply otherwise. Families do, however, need to know that the possibility exists, because even the possibility changes how they should think about timing, documentation, and liquidity.

The institution’s own release policy is the third gate. Even where authority is clear and tax issues are manageable, the custodian still has its own forms, review standards, residency rules, and operational requirements. It may require recent court certifications rather than older copies. It may want original signatures, specific tax forms, or in some cases a Medallion signature guarantee rather than ordinary notarization. It may allow the heir to receive the assets into a newly opened account, or it may insist on transfer out, liquidation, or another workflow more consistent with its compliance rules. None of this is unreasonable. It is simply not the way families think about the account while the owner is alive.

The decisive timeline in a cross-border estate is often not the legal timeline but the family timeline. Housing costs, school fees, travel, professional fees, and immediate living expenses do not wait for probate papers, translated documents, or tax clearance. In straightforward cases, transfers can move fairly quickly. In international estates, months are common, and the gap can be much longer when authority is contested, documents are foreign, or tax procedures need to be completed. Families therefore need separate liquidity outside the asset itself. Otherwise the estate may be solvent on paper and strained in practice.

One subtle mistake in international planning is to confuse investment diversification with jurisdiction diversification. A portfolio may be well diversified by issuer, sector, and geography, yet still be concentrated at the point where control has to change hands. A U.S. brokerage account holding global securities can feel globally diversified during life. At death, it is still one U.S. custodial problem.

The transfer path is governed by the system in which the asset sits, not by the countries represented inside the portfolio. A family can own companies all over the world and still depend on one legal environment, one custodian, and one administrative process to get the assets released. What feels balanced on a balance sheet can therefore turn out to be concentrated where it matters most.

Families sometimes respond by searching for a more international-looking wrapper: a regional trust, an offshore platform, a holding structure that appears to stand above jurisdictions. Sometimes that is appropriate. Sometimes it merely relocates the friction and adds another layer of reporting, custody, or tax analysis. A structure is not better because it sounds more international. It is better only if it leaves the eventual heir with a clear and workable transfer path.

Cross-border estates become coordination problems because death collapses professional boundaries. During life, the estate planner can focus on documents, the broker on custody, the tax adviser on filings, and local counsel on local law. After death, those distinctions stop mattering to the family. The family sees one estate and one urgent question: who can act, and when?

Fragmented expertise is not the same as coherent architecture. Each adviser may be doing sensible work within his or her lane. The difficulty is that inheritance problems rarely arrive in lanes. The probate lawyer may not know the brokerage firm’s inheritance workflow. The tax adviser may not be coordinating foreign translations or valuations. The investment adviser may understand the account but not the cross-border authority chain. None of this suggests bad advice. It suggests that many estates are assembled by discipline and only later exposed as systems.

Sequence matters more than families expect. The institution may not discuss release until authority is established. Authority may depend on foreign probate documents or trust papers. Tax filings may depend on valuations and asset inventories. If nobody owns the sequence, the heirs become the project manager by default. For a grieving spouse or adult child who lives outside the United States, that is usually the least suitable person to be managing it.

The most useful estate review begins by abandoning the owner’s vantage point. The owner is usually the person who understands the structure best, and also the one person who will not be there when it is tested. The proper question is not whether the owner can explain the estate. It is whether the surviving spouse, an adult child, or the executor could operate it with the information and authority available to them in the first week after death.

A useful review starts with a simple thought experiment: if death occurred tonight, who would call the U.S. custodian tomorrow morning, and what could that person actually prove? That exercise should identify where each asset legally sits, how it is titled, whether it passes by beneficiary designation, trust, or probate, and which institution actually holds it. Many families know the approximate portfolio value but not the legal route by which each part of it transfers. That is enough while the owner is alive. It is not enough for the people who inherit.

The review should then test the document chain. Who has the original estate documents? Where are the trust extracts, prior account statements, beneficiary forms, and contact details for the custodian’s estate team? If the death occurs abroad, who can obtain the death certificate, certified translations, and any further certification that may be needed? If probate is required, which lawyer is expected to obtain the authority documents, and in which jurisdiction? If the answer to any of these questions is “we will work it out later,” the estate is not yet operational.

Liquidity deserves its own review. A family should not assume that a U.S. brokerage account can fund immediate life simply because it is liquid in market terms. Market liquidity and estate liquidity are different things. If the account were tied up for six months, what cash would the family use instead? That question is rarely theoretical. It is often the one that reveals whether the structure protects the heirs or merely names them.

A final part of the review is coordination. Someone should know which adviser drafted the documents, who handles the U.S. tax side, who speaks to the custodian, who can help with foreign documentation, and who is responsible for moving the sequence forward. When relatively modest adjustments are made in advance - cleaner beneficiary designations, better document storage, a designated point of contact, a separate liquidity reserve - the future estate often becomes much simpler without any dramatic restructuring.

Most of the analysis above can be reduced to four questions.

Family consensus is not the same thing as legal authority. If the answer depends on a court appointment, a trustee certification, or some other step that has not yet occurred, the structure is less ready than it appears.

This is the practical test. Death certificates, authority documents, translations, certifications, tax forms, identity documents, and institution-specific paperwork are all manageable in the abstract. They are much less manageable when the family is overseas and no one has assembled the chain in advance.

The answer determines whether the estate has real resilience or only paper sufficiency. A family that depends on immediate access to the asset is far more exposed than a family that can tolerate delay.

If nobody clearly owns that handoff, the structure is relying on goodwill and improvisation. That sometimes works in domestic estates. In cross-border estates, it is a fragile assumption.

Usually yes. The harder question is not whether the beneficiary can inherit, but how the transfer will be administered and whether the firm will maintain the relationship in the same form once the new owner is abroad. Some custodians will transfer the assets into a newly opened account, some will require a different workflow, and some may limit what can be held or serviced based on the beneficiary’s country of residence.

No. The existence of U.S. estate-tax exposure usually turns on the decedent’s status and the nature and location of the asset, not simply on the heir’s foreign residence. Living abroad often creates administrative friction more reliably than it creates tax by itself.

There is no universal packet, which is part of the problem. Families often need a death certificate, proof of authority for the executor or trustee, identity documents, beneficiary or account-transfer paperwork, and tax forms. If the key documents were issued outside the United States, certified translations or further certifications may also be required.

Straightforward beneficiary cases can move reasonably quickly. Cross-border estates often do not. Once probate, foreign documentation, tax clearance, or institution-specific review enters the process, families should think in months rather than days and avoid planning around the best-case scenario.

No. Transfer-certificate procedures arise only in certain estates. The important point is not that every family will need one, but that the possibility should be screened early because it can materially affect timing, documentation, and liquidity planning.

Not always. Some firms are comfortable onboarding foreign heirs within defined parameters. Others may require assets to be moved to another institution, retitled in a different way, or liquidated before transfer. It is better to understand that policy while the owner is alive than to discover it after the account has already been frozen.

In the end, serious estate planning is not just a matter of having the right documents in a file. It is a matter of making transition possible. U.S. assets can be entirely sensible for internationally mobile families during life. The question is whether the people who survive the owner can move those assets from legal title into practical control without learning the system under stress.

A related difficulty appears in the other direction as well. When a U.S. person inherits non-U.S. assets, the problem may be less about access than about compatibility, especially where foreign pooled funds or trust structures create U.S. tax and reporting complications or where the local provider is unwilling to keep servicing a U.S. holder. That is a different article, but it rests on the same principle: receipt is not the same as usability.

Estate planning has done its job only when the heirs can actually operate the structure they inherit. If that cannot be said with confidence, the planning is not finished, no matter how orderly it may look while the owner is alive. For internationally mobile families, that test rarely arrives gradually. It tends to arrive all at once.

1. IRS - Transfer Certificate Requirements

2. IRS - Estate Tax for Nonresident Assets

If you’ve already ‘made it’ - and now want to make it count - we should talk.

We work with a maximum of 12 new families, executives, or founders each year to simplify complexity, and organise our client intake quarterly.